Knowledge Centre

Canadian Dollar Limbos Lower

October 2015

The global financial markets are intertwined into one gigantic and convoluted web. Nowhere is this truer than with the relationship between currencies and bond spreads, which are the difference between various country's interest rates. Bond yield differentials play a significant role in determining the direction of a currency and has more influence on the direction of a currency move than the underlying bond yields themselves.

Currency valuations reflect economic fundamentals over time, although there can be temporary imbalances that disturb the underlying fundamentals. The price of currencies can be impacted by the monetary policy decisions of central banks around the world but central banks, like the Bank of Canada, only administer short term interest rates or the front end of the yield curve. It is market forces which drive market sentiment and ultimately determine the yields on longer dated bonds. It is the longer dated bonds that have 10 or more years to maturity that are the primary force for determining exchange rates.

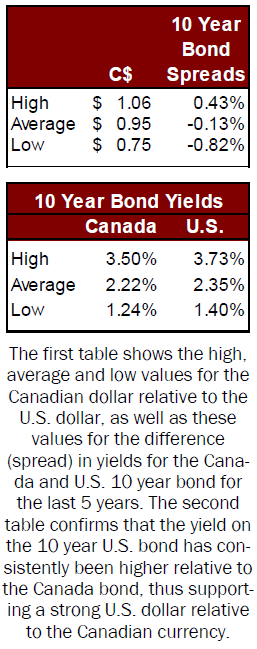

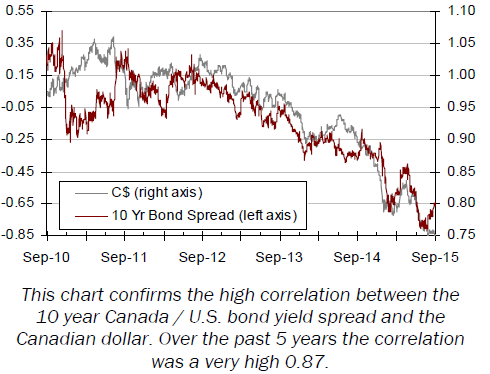

Bond yields differentials usually move in tandem with the corresponding country's currency as capital flows are attracted to higher yielding currencies. As a general rule of thumb, when the yield spread widens in favor of a country then its currency will appreciate more than other currencies. While it is not uncommon for currency movements to lag as much as a year after interest rate differentials have moved significantly, this is not the case between Canada and the U.S. Quite simply, the Canadian and U.S. government 10 year bond spreads accurately dictate the direction of the Canadian dollar better than any other indicator. As the chart to the right and data to the left indicate the relationship between the 10 year bond spread and the Canadian dollar is highly connected. Over the past 5 years of daily activity the correlation is 0.87 (with 1.0 indicating perfect correlation and 0.0 means no correlation). To further put this in perspective the correlation between the 10 year Government of Canada bond yields on their own and Canadian dollar is 0.56; while the correlation the 10 year U.S. Treasury bond yield and Canadian dollar is only 0.14. Interestingly, many pundits call the Canadian dollar a "petro-currency" because of oil's big influence on our economy but the correlation between the currency and the price of oil is only 0.25.

Canadian and U.S. interest rates are low in absolute terms but the lower Canada's interest rates go relative to the U.S. then the lower our dollar will go. While there certainly appears to be a concerted effort to stimulate the Canadian economy through a lower Canadian dollar it could risk a currency crisis and a Canadian dollar in free fall below the 2003 low. The problem is that once momentum is established and a trend develops, it is very hard to reverse its course. In the past five years the Canadian dollar peaked out at $1.06 and is currently at $0.75. This is a 29% depreciation and there is no indication that market sentiment is going to change meaningfully to alter this course. The only real question is "how low will it go?"

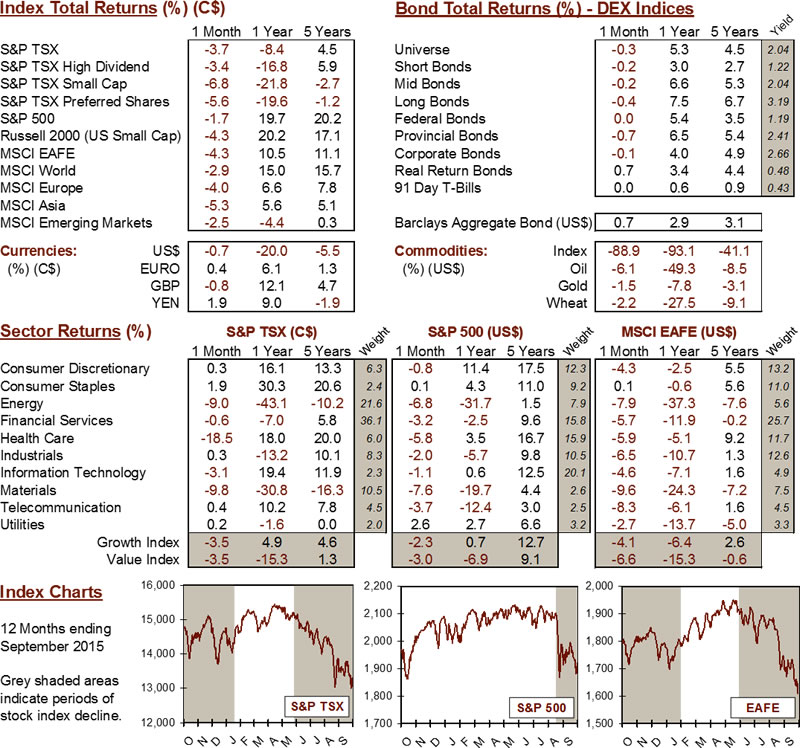

MARKET DATA

This report may contain forward looking statements. Forward looking statements are not guarantees of future performance as actual events and results could differ materially from those expressed or implied. The information in this publication does not constitute investment advice by Provisus Wealth Management Limited and is provided for informational purposes only and therefore is not an offer to buy or sell securities. Past performance may not be indicative of future results. While every effort has been made to ensure the correctness of the numbers and data presented, Provisus Wealth Management does not warrant the accuracy of the data in this publication. This publication is for informational purposes only.

Contact Us

"*" indicates required fields

18 King St. East Suite 303

Toronto, ON

M5C 1C4