Knowledge Centre

Do Rising Short Rates Signal Pain for Bonds?

November 2021

Interest rates could be on the rise in Canada next year as the Bank of Canada reverses its long term policy of stimulating the economy to offset the debilitating impact of COVID-19. The general consensus is that sometime during 2022 short term interest rates will be going up. What impact will this have for the typical client’s portfolio? We all learned in our first investment course that rising interest rates are bad for bonds. In fact, history provides a different perspective concerning the impact of rising interest rates on a broadly diversified bond portfolio.

When analyzing the past experience of bond investors under different interest rate scenarios, it is clear that a bear market in bonds is quite different from a bear market in stocks. Unlike stocks, where the common definition of a bear market is a 20% decline in prices, most investors believe a bear market in bonds is simply a period of negative returns. The past 50 years of return data has shown that these periods are few and far between with only 5 calendar years of negative performance. The average annual decline in those years was -2.86%; with the largest drop being -4.53% in 1974 (although YTD 2021 could potentially set a new record low as bonds are returning -4.96% as at October 31, 2021).

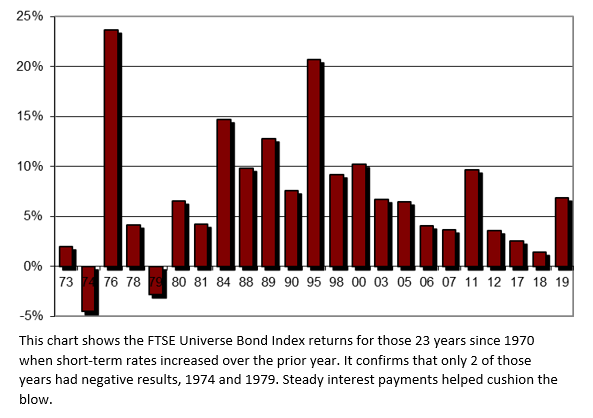

The chart to the right shows that increases in interest rates at the short end of the yield curve have not necessarily hurt most bond portfolios. Since 1970 there have been 23 years where the short term or 91 Day T-Bill yields have increased over the prior year. The chart shows the calendar year performance for the FTSE Universe Bond Index, the broadest and most widely used measure of government and corporate bonds in Canada, for those years where short term rates increased. The first thing that jumps out is that there are only 2 years with negative results, 1974 and 1979; and as previously mentioned the -4.53% return in 1974 was the worst annual bond performance of the last 50 years. The average annual performance over the 18 years was 7.08% which is only slightly less than the 8.56% average annual return over the last 5 decades.

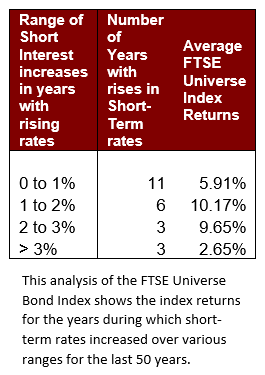

Even when rates are rising across the maturity spectrum, it is unusual to suffer large losses in bonds. When both short term and longer term rates increase together it is more likely that bonds will see low or slightly negative performance. As the data illustrates, in periods where short term rates increase between 1 and 3%, rising short rates can have a positive impact on bond results. Even during periods where short rates were rising at a rate of greater than 3%, bond investors still managed to realize positive returns on average.

So far in 2021, short term rates have fallen due to the funding of emergency stimulus to fight the impact COVID-19 has had on the Canadian economy. Since the Bank of Canada’s priority is to keep inflation low, the likelihood of the Bank triggering a surge in interest rates without clear warning is not very high. Despite the potential for rising interest rates, investors should view bonds as a diversifier for the riskier assets in their portfolio and not necessarily view rising rates as a source of risk . Most diversified, long term investors should not view weakness in the bond market with the same apprehension as an equity bear market. In general investors should look to bonds for a stable income and to protect against disaster (something which they did well during the financial crisis). Bonds are an asset class capable of storing value, providing liquidity and most importantly, providing positive returns in most economic environments.

MARKET DATA

This report may contain forward looking statements. Forward looking statements are not guarantees of future performance as actual events and results could differ materially from those expressed or implied. The information in this publication does not constitute investment advice by Provisus Wealth Management Limited and is provided for informational purposes only and therefore is not an offer to buy or sell securities. Past performance may not be indicative of future results. While every effort has been made to ensure the correctness of the numbers and data presented, Provisus Wealth Management does not warrant the accuracy of the data in this publication. This publication is for informational purposes only.

Contact Us

18 King St. East Suite 303

Toronto, ON

M5C 1C4