Knowledge Centre

Retirement Income On Steroids

October 2017

Short term interest rates are near 60 year lows which makes it hard for fixed income investors to earn a decent income. Couple this with the fact that the average investor has an aversion to investing in long term bonds because of the belief that higher interest rates are on the horizon and it becomes nearly impossible to earn much more than money market rates. So what are the options for clients looking for good yields while being able to take advantage of higher returns in the future?

With over $300 billion in assets, Guaranteed Investment Certificates (GICs) account for a huge share of fixed income sales in Canada. This is due to the advantages that many investors feel GICs offer over bonds: a predictable and guaranteed income stream, the principal value won't decline and no fees mean every penny earned is theirs to keep. For these benefits clients are subjected to returns that can be low and, after inflation, the returns are actually negative. This is not a great situation as people are living longer. Sometimes the safety investors are seeking becomes just another form of risk.

After GICs, bonds are the next popular vehicle in adding returns to an investor's portfolio as they have very different characteristics but do offer distinct advantages. Interest rate changes affect bond values so that as rates fall, bond prices increase and as rates rise, prices fall. However, if held to maturity bonds repay the full principal. Another essential difference is liquidity. Bonds can be bought or sold at any time with price determined by each bond's individual characteristics and current market conditions. While bond returns are impacted by the cost of purchasing and managing the portfolio, this can be offset by the higher returns bonds can achieve. They offer the distinct possibility of higher yields and capital gains.

Taking it one step further and incorporating other types of fixed income vehicles into the mix can be quite rewarding for conservative investors. For example, constructing an optimized High Yield Fixed Income portfolio consisting 15% of a 10 year Corporate Bond Ladder, 7.5% REITs, 20% High Yield Bonds, 15% High Yield ETFs, 20% Mortgages and 22.5% Fixed Income Hedge Funds leads to a very attractive alternative. Certainly the degree of risk investors assume with this type of portfolio are higher, but so is the potential for greater returns. The real question is, is it worth it?

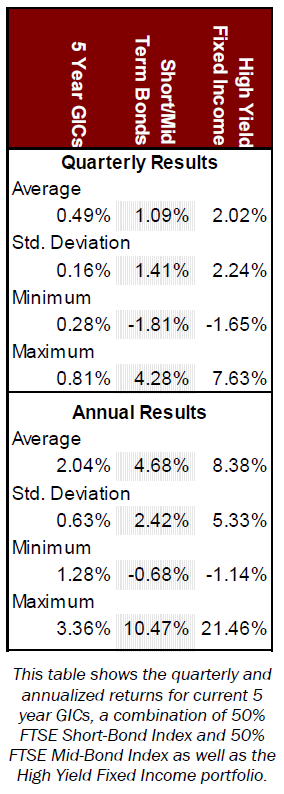

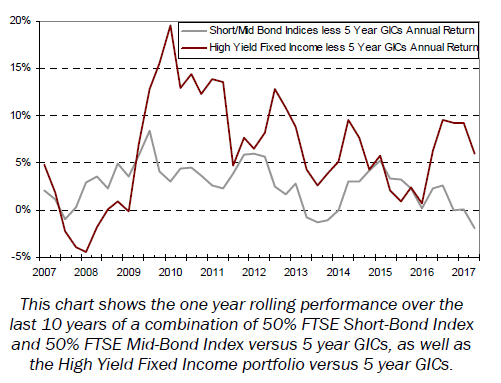

Given current low interest rates this may be a good time to consider these strategies. Current 5 year GIC rates (based upon the average rates of the Schedule A chartered banks) are 1.6%. Using bonds with a similar term structure (represented by 50% FTSE Short-Bond Index and 50% FTSE Mid-Bond Index) shows how an all bond portfolio would perform. While the returns for the outlined High Yield Fixed Income portfolio is clearly superior. As the chart above shows, over the past 10 years the one year rolling performance of these two portfolios consistently produce higher returns when compared to 5 year GICs (outperforming 83.3% and 88.1% of the time, respectively). The data to the left shows these advantages both on a quarterly and annual basis; while doing so with very low correlation to GICs of 0.22 and -0.24 respectively.

With today's very low yields and increasing interest rates, investor returns on GICs after inflation, fees and taxes are minimal. So unless investors are comfortable with only safe harbour investments and unconcerned with the less than stellar returns going forward, the only realistic solution is to explore other options. The decision to be safe is making many investors less safe and creating a whole new level of risk, running out of money. With this situation bearing down on many investors, the proposed High Yield Fixed Income structure is a solution that plays it safe, but still generates meaningful returns.

MARKET DATA

This report may contain forward looking statements. Forward looking statements are not guarantees of future performance as actual events and results could differ materially from those expressed or implied. The information in this publication does not constitute investment advice by Provisus Wealth Management Limited and is provided for informational purposes only and therefore is not an offer to buy or sell securities. Past performance may not be indicative of future results. While every effort has been made to ensure the correctness of the numbers and data presented, Provisus Wealth Management does not warrant the accuracy of the data in this publication. This publication is for informational purposes only.

Contact Us

"*" indicates required fields

18 King St. East Suite 303

Toronto, ON

M5C 1C4